Since July of 2017 the Bank of Canada has raised interest rates five times. And up until December of 2018 the Bank of Canada maintained that its key bank rate would need to continue to increase until it got to their toward its estimated “neutral range,” of between 2 ½% and 3 ½%. That would have meant that rates would need to go up by an additional ¾% to 1 ½% higher than today’s rate of 1 ¾%.

In December of 2018 the Bank of Canada maintained their rate at 1 ¾% and in their comments indicated that rates may not go up as quickly as they expected. They based this on the fact that the Canadian economy was slowing as a result of lower oil prices, weaker consumer spending and a slowing housing market.

At the first meeting of 2019 the Bank of Canada again decided to keep their overnight interest rate at 1 ¾% and mentioned the same concerns as they had mentioned in December.

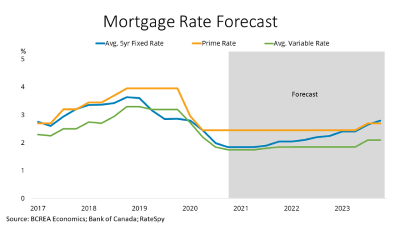

So what happens for the rest of 2019? Predicting where interest rates are headed is always a challenge and if you look at the chart below you can see what the economists at the banks think. For the most part it seems that most lenders are saying that the increase in interest rates will slow in 2019 and that the increase will be between ¼% and ½%. It is in 2020 that you start to see more of a split in the predictions with some analysts predicting that rates could actually drop by the end of 2020. This drop in rates is based on the risk that there could be a recession at some point which would see the Bank of Canada drop rates to help get the economy going again.

|

2019 |

|

2020 |

| Lender |

Q1 |

Q2 |

Q3 |

Q4 |

|

Q1 |

Q2 |

Q3 |

Q4 |

|

|

|

|

|

|

|

|

|

|

| CIBC |

1.75 |

1.75 |

2.00 |

2.00 |

|

2.00 |

2.00 |

2.00 |

2.00 |

| Desjardins |

1.75 |

1.75 |

2.00 |

2.00 |

|

2.25 |

2.25 |

2.25 |

2.00 |

| National Bank |

1.75 |

1.75 |

2.00 |

2.25 |

|

2.25 |

2.25 |

2.25 |

2.00 |

| RBC |

1.75 |

2.00 |

2.25 |

2.25 |

|

2.50 |

2.50 |

2.50 |

2.50 |

| Scotia |

1.75 |

2.00 |

2.25 |

2.50 |

|

2.75 |

2.75 |

2.75 |

2.75 |

| TD |

2.00 |

2.00 |

2.25 |

2.25 |

|

2.50 |

2.50 |

2.50 |

2.50 |

Looking at the bond markets provides additional support for the idea that interest rates will not be moving higher by a significant amount. Government of Canada bonds are as of January 9th yielding 1.91% for a two year term, 1.91% for a five year term and 1.98% for a ten year term. The bond traders are not asking for any premium to lend money out for longer which is a sign they don’t expect much of a change in interest rates.

So what does that mean for you? If your mortgage is up for renewal you may want to consider either a variable rate or maybe a shorter fixed term in the two to three year range. One of the things I can do for you is prepare a comparison of the different options to help you decide which is best for you.

If you have any questions about your mortgage call me at 604-961-2400.

Lawrie